Yesterday the 10 year TIPS closed at an all time low of -0.33%. The flight to safety due to the Greek crisis pushes TIPS down because 10 year exceptions of inflation are not really being affected by Greece. ( TIPS + inflation expectation = Nominal treasury yield ). Fixed income investors are going to have to tolerate an “extended period” of low returns. If you want to see this data in a nice convenient form look under the fixed income > historic yields tab and select TIPS.

Archive for the ‘Market commentary’ Category

The records keep falling … the oil/gas price ratio hit another all time high on the 19th at 9.29 (Cushing closed at $102.58/bbl and Henry gas closed at $1.90/mmBtu). The gas price is the equivalent of oil at $11.02/bbl.

Meanwhile, low gas prices are driving the price paid to older renewable producer in California to near record low levels. In PG&E the April price for “Short Run Avoided Cost” is 2.7 cents/kWh. IMO prices this low will cause some renewable facilities to shut in, unable to recover operating costs, much less insurance or property taxes. It’s ironic for a state that is imposing a 33% RPS standard and implementing a cap and trade system to have a pricing mechanism that will force some production to, effectively, be flared.

For the first time the price of crude at Cushing Oklahoma is over 8 times (on an energy basis) the price of natural gas at Henry Louisiana. And Cushing is below world markets as measured by Brent. Small wonder that automakers are starting to produce duel fueled gasoline / natural gas vehicles. With this wide a price differential it should be possible to get natural gas to the tank for a savings over gasoline.

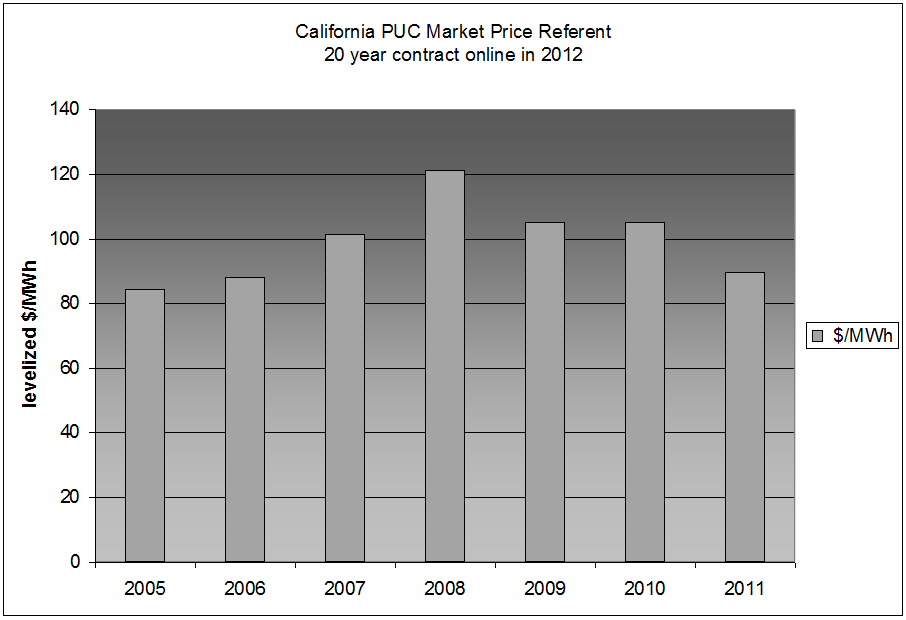

Since 2005 California’s Public Utilities Commission has been publishing a Market Price Referent (MPR) based on a 500 MW combined cycle plant. The MPR serves as a benchmark for renewable projects and has been used since 2007 as the basis of contracts offered pursuant to the Feed In Tarriff (FIT) program. Predictably, since the MPR is based on a gas plant the price moves up with the outlook for gas and also moves down with the outlook for gas. The chart below illustrates this relationship:

Note that the CPUC didn’t update the MPR in 2010 as gas prices were falling creating the “plateau” in 2009/2010. If the MPR were updated now I would expect another drop for the simple reason the gas prices used in 2011 are unrealistic. The 2011 NYMEX monthly contracts averaged to yield a 2012 price of $4.84/mmBtu. As of today, the Mar – Dec 2012 contracts averaged $3.05 and the monthly contract didn’t exceed $4.84 until Dec 2016.

So why does this matter if California has mandated 33% RPS and FERC has allowed avoided cost to be set based on tranches of RPS requirements?

The oil gas ratio hit a new record high today with gas trading at $3.11/mmBtu and WTI going for $101.25/bbl yielding an energy ratio of 5.61. In simple terms this means gas is trading at the equivalent of $18.05/bbl crude.

The market is starting to notice this rapid shift in natural gas economics. Back on Dec 10 I mentioned a few of the sectors, such as chemical processing, that would be likely winners due to lower priced gas. Companies are now starting to announce their plans to build new plants. Royal Dutch Shell PLC is planing an ethylene plant in the Appalachian region, Nucor is building a gas fired iron plant in Louisiana, Dow Chemical Co. is planning two new chemical facilities in the Gulf coast, and CF Industies is planning to boost its ferterlizer production made from gas. (WSJ, 12/27/2011, A3) . All due to relatively low gas prices. If LNG importers are not able to “reverse to flow” and turn into LNG exporters, then the price of gas can stay low until domestic consumption has a chance to absorb these lower cost supplies.

One of the other sectors that should benefit from the relatively high oil/gas ratio is the CNG (compressed natural gas) transportation buisness. In October I analyzed Clean Energy Fuels’ [CLNE] stock performance relative to the energy ratio and couldn’t really see any coorelation between the fundamental driver of their business (the oil/gas ratio) and their stock price. Checking back today I’m still not seeing any sustained improvement in the company’s stock price. So I’m still looking for the breakthrough in the transportation business.

In other news, shale gas is certainly affecting the price of electricity, both spot prices and prices offered for term contracts for renewables. In the western US, on-peak spot prices in southern California today were $30.37 $/MWh….lower then they were 30 years ago in 1981 when our company (www.henwoodassociates.com) started producing power. And the natural gas based market reference price (MRP) used by the California PUC for evaluating renewable projects is off about 15% from the last MRP posted by the CPUC.

While this is happening the solar sector is having problems with oversupply and a softening market. The oversupply is drivien by the rapid increase in Chinese production (including two IPOs in October and November – Changzhou Almaden and Sungrow Power). Coupled with German demand for 2011 reported to be 29% below 2010 levels two German producers, Solar Millennium and Solon SE filed for insolvency this month. The supply/demand combination is also driving layoff such at those reported at SMA, Suntech, and First Solar. And stock prices for solar companies, as measured by the solar ETFs KWT and TAN, have dropped by over 60% YTD and their market cap has fallen below the $70 million level that was related to me as a break-even size for an ETF. In fact, all of the sponsors of sector specific ETFS – KWT, TAN, FAN, PWND, GRID – are losing money on their offerings if this is still the break-even number. Which one will close up first like the progressive transportation ETF did in 2010?

How much of the market woes facing solar producers stems from gas competition? I’m not aware of any analysis of the relationship of subsidies and RPS mandates to gas prices in the US, but reason tells us there must be some connection beyond a mere correlation of gas prices and solar woes.

I think this is just the start of the disruptions caused by low gas prices. On a very small scale our company is affected in contract renewals and the prospects of lower electric prices/subsidies for new project development. Many other businesses will be forced to adapt and potentially sooner then anyone expects.

It’s officially winter and Henry hub gas futures are below $3.20/mmBtu. With WTI oil near $100 / bbl the oil/gas ratio hit an all time high today of 5.43.

On January 13, 1994 the ratio(*) of the price of oil to the price of natural gas was 1.14. Today it hit a 17 year record high of 5.26. Gas traded at $3.28 today, just 21% of the $15.38 / mmBtu it traded for on December 13, 2005. Shale gas is providing gas in volume at moderate cost driving this record high price disparity.

IMO, the impact of moderately priced gas hasn’t been factored into energy policy to any great extent. Nor has the balance of the energy market had time to react. And the media hasn’t realized this is happening.

But there should be many winners – combined cycle generation, CNG vehicles, chemical processing that uses gas, and gas consumers. Why isn’t there a stamped into new fleet conversions to CNG….it’s way cheaper than gasoline?

The will also be disruption, – coal, climate change strategies, and renewable generation will be impacted. Why sequester carbon when you can replace a coal plant with a super efficient combined cycle plant and emit 50% less CO2?

My prediction for 2012 – renewable electric generation, and its subsidies, feels some competitive heat in the US.

(*) The energy price ratio is the price of crude on a $/mmBtu basis divided by the price of natural gas on a $/mmBtu. The crude prices used are the front month NYMEX contract for WTI crude at Cushing Oklahoma. The $ per barrel price is converted to $/mmBtu using 5.8 mmBtu / bbl. The gas price used is the front month NYMEX contract for natural gas at Henry Hub Louisiana.

The California Air Resources Board today unveiled Advanced Clean Car Regulations aimed at reducing smog causing emissions and addressing concerns about global warming. Somehow the ARB has concluded, in at least one scenario, that about 35% of of light duty vehicle in 2040 will be hydrogen fuel cell cars. And when more than 10,000 of these cars are sold in an air basin the Clean Fuels Outlet regulation will require the construction of hydrogen fueling stations. But don’t worry, “Staff projects that, with high station utilization, fuel providers will be able to sell hydrogen at an affordable price and realize a return on their investment within three to four years.”

In contrast, Exxon Mobil’s 2012 The Outlook for Energy: A View to 2040, doesn’t even mention hydrogen fuel cell cars playing a part in 2040.

The ARB apparently still remembers Governor Schwarzenegger’s Hydrogen Highway vision. No one else seems to.

…the 5 year TIPS traded at an all time low real yield today of -1.047%. The 10 year didn’t quite hit a record but it traded at a real yield of -0.64% . The last time the TIPS yields hit a record low was on August 10, the day the DOW dropped 508 points. In contrast, today the DOW fell a modest 61 points and is over 1000 points higher than it was August 10. In August money was moving into the safety of US Treasuries driving down their yields and carrying the TIPS down with them. Today, it looks like the ECB rate cut put pressure on Treasuries with a similar effect. The TIPS may have lower to go still. If inflation expectations click upward, and the central banks constrain nominal rates, then TIPS will go lower. Amazing, a very safe way to lose money in real terms.

This sector defines investment risk. Not only has Evergreen Solar, Inc. [ESLR] filed for bankruptcy, investors in another high visibility solar developer have been saddled with a 72% loss over the last week. In a massive shift that has to shake confidence in the company, Germany’s Solar Millennium AG [S2M.DE] announced on Thursday said it will convert the first 500 megawatts of its 1,000 MW Blythe solar power plant in the Mojave desert to PV. It will decide what technology to use for the second half of the project at a later date. Nor has it revealed the charge it will need to take due to the shift.

It’s not just these companies. The two solar sector specific ETFs [KWT and TAN] have lost 36.8% and 33.2% respectively this year. This is about double the loss broad-based market indices have suffered and lead the losses across all the clean energy ETFs and mutual funds. In fact these losses have depressed the size of the sector specific ETFs for wind, solar, and smart grid to where only the Guggenheim Solar ETF [TAN] has a market cap greater than $100 million. The other four ETFs market caps are below a rule of thumb $70 million threshold required for the ETF sponsor to make money. So I wouldn’t be surprised to see some of these ETFs shut down like the clean transportation ETF [PTRP] did last December.

That said, solar companies may be great technologists with good products. With falling panel prices it looks like PV is on track to wipe out solar thermal projects and is making progress on being grid competitive. Of course, in the US with natural gas prices constrained by the technological breakthrough that brought about shale gas, the bar for solar PV is being raised. Whether solar can reach parity (and without the support of creative ratemaking that turns $4/mmBtu gas into 20 cents/kWh power in the summer) is still not answered. But if so, solar companies with depressed stock prices may turn into good investments.

Disclosures: none